It is understood that in 2015, the market size of China's chronic disease medicine market was 732.3 billion yuan, a year-on-year increase of 7.3%, accounting for 53.3% of the total pharmaceutical market. In 2016, the market for chronic disease drugs expanded to 79.4 billion yuan.

For pharmaceutical companies, chronic disease medication is undoubtedly a "big cake." In fact, not only is the sale of medicines, the pharmaceutical companies are more responsible for the slower disease education, capacity service, brand output and other dimensions in the management of chronic diseases.

After the medical representatives have become a thing of the past, how to make their own brands seize the "mind" of customers has become the force of major pharmaceutical companies. In order to open up the industrial chain from drugs to patients, especially in the face of chronic diseases, which are almost the only drugs that need to be taken for life, pharmaceutical companies are using Internet technology to build a chronic disease management network related to their core business lines.

Through the chronic disease service, the path of channel exploration is becoming a common consensus and practice for pharmaceutical companies.

The arterial network combed the layout of 18 domestic and foreign pharmaceutical companies in the management of chronic diseases to explore the performance of pharmaceutical companies in the chronic disease management market and the effects of the services involved.

Our main findings are:

1. Drug compliance is a big market opportunity for pharmaceutical companies;

2. The service attributes of pharmaceutical companies are weak, and most drug companies spend most of their services on chronic diseases.

3. Driven by policies and markets, the actions of pharmaceutical companies in chronic disease services are concentrated in the two years from 2015 to 2016;

4. The service layout of pharmaceutical companies is usually related to their own business lines, and diabetes is a “big familyâ€;

5. More than half of pharmaceutical companies conduct services in cooperation with e-commerce, Internet medical platforms, and chronic disease management APPs;

6. "Internet platform, intelligent hardware, offline services" ranked the top three in the form of chronic drug service.

The core of chronic disease management is patient compliance

As far as the overall market conditions are concerned, the growth rate of the pharmaceutical market is slowing down and the market for chronic diseases is expanding. With the continuous advancement and deepening of the reform of the medical and health system, the comprehensive promotion of policies such as medical insurance payment reform, grading diagnosis and treatment, consistency evaluation and medical separation, the state has continued to strengthen the control over drug prices, and the overall price of drugs has shown a downward trend. All aspects of the pharmaceutical industry have a greater impact. If the company fails to cope with the drug price reduction policy and fails to seize the market opportunity brought by the price drop and market expansion, effectively expanding the sales scale will affect the company's profitability.

Therefore, pharmaceutical companies have begun to use the chronic disease field that requires long-term medication, and return the chronic disease management and doctors and patient education that they are not good at to the market and new technical means.

The main goals of chronic disease management include: patient education, instructional use, doctor education, user interaction, and long-term follow-up. At present, there are three aspects to the pain point of chronic disease management:

First, the problem of doctor motivation. As mentioned in the book "Innovator's Prescription", the biggest problem with the business model for chronic diseases is that doctors and hospitals are engaged in chronic disease management. This is a long-term business model for the treatment of acute diseases, and it will be used for the management of chronic diseases. It is not worth the candle. As far as foreign medical insurance is concerned, insurance will pay for the patient's disease diagnosis and treatment, and “will not pay for the doctor before the onset of illnessâ€. In the management of chronic disease, doctors do not receive the corresponding fees for providing services to maintain patient compliance. This is the biggest problem for doctors lacking the motivation to manage chronic diseases.

The second is the issue of compliance. At present, China has entered a high-burden period of chronic diseases, and it has the characteristics of "a large number of patients, high medical costs, long illness time, and large service demand." Chronic diseases last for a long time, and drugs can alleviate the disease to some extent. But the core of the key, the recipient lies in the patient, the compliance of chronic disease management requires patients to establish good living habits, even to fight against the bad habits of the previous, in this process often need to receive treatment as required, frequent key to the body Indicators are monitored and reviewed. At the heart of chronic disease management is effective patient education and compliance management.

The third is the payment problem. Here, using data from Latitude Health's research conducted in 2016, data shows that only 28% of users are willing to pay for chronic disease management, and 67% of users are willing to pay less than 500 yuan a year. The effect of chronic disease is difficult to assess, can not be characterized according to the treatment of acute diseases, the direct economic link with medical insurance control fees is not clear, and the chronic disease management market is not standardized, etc., it is difficult to be included in the scope of reimbursement. At present, the financial pressure on medical insurance continues to increase, and some medical outflows have already appeared in the medical insurance deficit. With the expansion of the slow patient population, if the management of chronic diseases is to be included in the scope of medical insurance payment, it will inevitably be a small expenditure. The long-term demand for drugs and treatments makes chronic patients often have a large economic burden.

Lack of patient compliance, low efficiency of doctor management, and weak willingness to pay for users make it difficult to become a separate industry. Given the growing trend of chronic drugs and the demand for sales by pharmaceutical companies, pharmaceutical companies may be the most chronically ill. Good "buy side".

Pharmacy's analysis of chronic disease service layout: from medicine to overall solution

Below, the arterial network counts the layout of 11 domestic listed pharmaceutical companies and 7 multinational pharmaceutical companies in the provision of chronic disease services. Because it is collected through public information and listed company annual reports, only typical cooperation projects are listed.

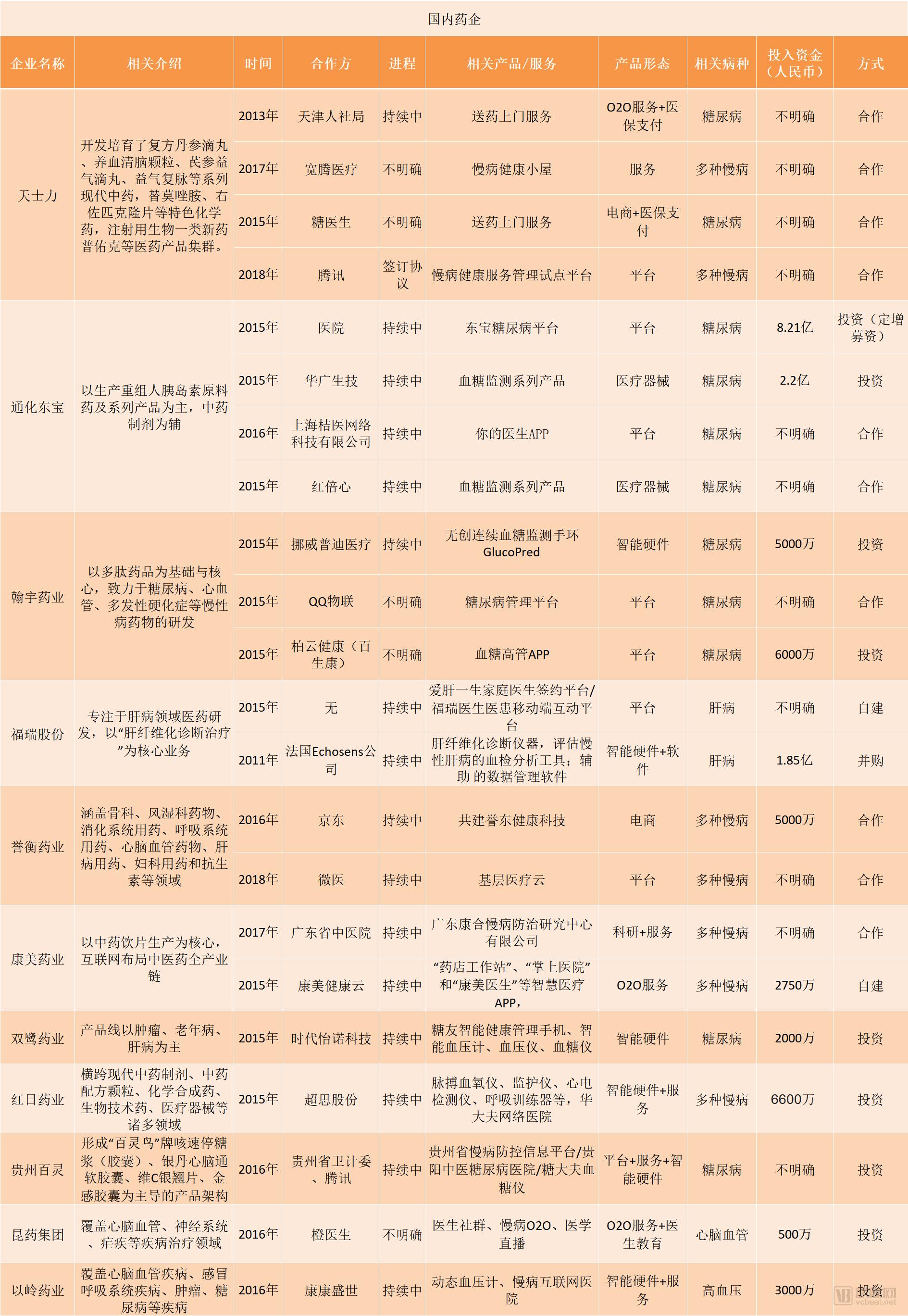

Table 1: Layout of chronic disease services in domestic pharmaceutical companies (data source: annual report of enterprises, public search, finishing: arterial network)

Table 2: Layout of chronic diseases in multinational pharmaceutical companies (data source: public search, organization: arterial network)

*Note: In the above table, the statistics of the multinational pharmaceutical companies refer to the chronic disease service projects in China. If a project cannot be queried on the official website, or the product activity rate is low, there is no updated iteration version, or even only the news of the initial exposure of the cooperation, the process is considered unclear.

Figure 1 Distribution of the chronicle service layout project of pharmaceutical companies

Figure 2 Sales revenue and growth rate of pharmaceutical companies in 2012-2017 (Source: Kangmei Pharmaceutical 2017 Annual Report)

From the perspective of the year, the chronic disease projects of pharmaceutical companies are concentrated in 2015 and beyond. Compared with the sales revenue and growth rate of pharmaceutical companies in the past five years, the overall development of “V†shape, while in 2015 is the lowest growth rate of pharmaceutical companies, a decrease of about 4 percentage points from 2014.

For the pharmaceutical industry, this year is a year of shocks, the implementation of new national tenders, the regulation of drug-to-market policies, and the reform of the medical insurance payment system. Among the many medical policies, these are the most influential and important. The force of the policy has almost come to a point of focus - the price of medicines, and the co-ordination of various policies will eventually lead to a substantial reduction in drug prices.

2015 is not a good year for pharmaceutical companies, especially multinational pharmaceutical companies. According to the report of Xinkangjie, due to the pressure of bidding and price limit, in the process of bidding for drugs in Zhejiang, Hunan, Fujian and other places, foreign-funded pharmaceutical companies abandoned the standard in large scale, and after the first batch of national drug prices, the two foreign-invested original drugs were greatly reduced. above 50.

At the two sessions in 2016, “Internet + chronic disease management†was heatedly debated by NPC deputies and CPPCC members, and multinational pharmaceutical giants focused on the primary battlefield of chronic disease and chronic disease management – ​​the primary medical market. Slow disease management is seen by investors as a gold mine for mobile medicine . Internet companies such as pharmaceutical companies, medical device factories, and BAT have entered the field in various forms.

As shown in Table 1, most of the actions of drug companies such as Hanyu Pharmaceutical and Tonghua Dongbao in the chronic disease service are concentrated in the two years from 2015 to 2016, mainly driven by policies and markets. In 2017 and 2018, the main form of medical innovation, Internet medical care, is far less hot than the previous two years, and the chronic disease policy is also concentrated on primary medical care based on graded diagnosis and treatment. Therefore, the use of the Internet to construct chronic disease services in the past two years is more important. less.

Figure 3 Distribution of chronic disease services in pharmaceutical companies involves the distribution of disease types

Insulin is the last line of defense for patients with diabetes. It is a must-have and irreplaceable drug in the middle and late stages. Once patients have poor long-term control of blood glucose, it is likely to cause retinopathy, chronic renal failure, neuropathy, cardiovascular disease and other common complications of type 2 diabetes. In severe cases, diabetic foot may even lead to the risk of amputation.

Among the chronic diseases that pharmaceutical companies are involved in, diabetes accounts for the first place, reaching 50%, which is related to the pain point of traditional diabetes treatment. The most intimate drug related to diabetes is insulin. Traditional diabetes treatment and monitoring is less than once a day, and more than 3-4 times blood collection and injection, which is very "anti-human."

According to domestic sample hospital data, insulin accounts for 40% of domestic diabetes medications. Considering that sample hospitals are concentrated in the top three hospitals in large and medium-sized cities, and the use of insulin in China's primary layer is lower, the actual proportion of diabetes medication in China is much lower than 40. %. Whether it is the "Hundred Sugar Battle" around 2015, or the layout of pharmaceutical companies in diabetes, it is because the patients with diabetes need to have higher compliance.

Blood glucose monitoring, medication management, doctor advice, etc., improve patient visit rate and user stickiness, and lay the foundation for insulin product introduction, which may be a major reason for pharmaceutical companies to pay for diabetes management services.

On the other hand, the layout of pharmaceutical companies in diabetes is also related to their own business lines. For example, the sales of recombinant human insulin APIs of Tonghua Dongbao have accounted for more than 20% of the market share, ranking second (according to Tonghua Dongbao 2017). Annual report data), multinational drug companies Novo Nordisk, Eli Lilly, Sanofi is a major drug for diabetes drugs. A report by Mobihealthnews in 2015 showed: “Let patients take prescription drugs to help the medical system save nearly $290 billion, which means that sales of pharmaceutical companies will increase. Scripps Health Center cardiologists And Internet medical advocate Dr. Eric Topol believes that pharmaceutical companies have largely missed the opportunities brought about by drug compliance. "Pharmaceutical companies often miss the part of the market that is not given up because of compliance. Therefore, the layout of diabetes services, For pharmaceutical companies, it is an initiative to expand the product sales chain.

Figure 4 Distribution of chronic disease service layout in pharmaceutical enterprises

As can be seen from Figure 4, 50% of the ways in which pharmaceutical companies lay out chronic disease services are carried out in a cooperative manner. This is not unrelated to the fact that most of the drug companies themselves are slow-moving, and they are transmitted at the end of 2015. Novo Nordisk disbanded all education commissioners across the country and gave up the model of offline patient education.

The pharmaceutical company is the end closest to the patient, but the medical service is not strong. This is also related to the “identity†of the pharmaceutical company. If the pharmaceutical company engages in patient education from the purpose of sales, the trust of doctors and patients will inevitably be affected; When marketing is detached, it will become a simple consulting service for patients who use drugs, which often costs a lot of money.

The major multinational pharmaceutical companies are usually keen to cooperate in the management of chronic diseases. The seven chronic drug companies in AstraZeneca, Sanofi and Lilly are almost all cooperative in China. The cooperation targets include e-commerce, Internet medical platform and chronic disease management APP. The effect that cooperation often wants to achieve is to use their respective advantages to achieve the effect of “1+1>2â€. For example, in November 2017, according to its official semi-annual pilot operation data, the company has interacted with the Tencent and Liyuan Parks in the past six months. According to the official data released by the company, the patient interacted with the team of the Care Center through 200,000 times. The patient's blood glucose test totaled 150,000 times, and the proportion of stable blood glucose increased by 15%-20%, delaying the onset of complications.

Figure 5 Distribution of morphological distribution of chronic disease services in pharmaceutical companies

Note: Since the chronic disease services involved in pharmaceutical companies usually have multiple forms of overlap, such as “O2O service + medical insurance paymentâ€, this statistic counts all the forms involved in the service project separately. If an event involves two forms of “O2O service + medical insurance paymentâ€, it will be counted separately under each option.

Based on the above statistics, there are several types of partners that are most favored by pharmaceutical companies:

The first is the Internet platform (illustrated as a mobile platform). Among the 18 pharmaceutical companies, 12 companies have a chronic disease service business that is carried out on an Internet platform.

For pharmaceutical companies, the premise of adapting to the Internet environment is to change the marketing method and focus on patients. Therefore, building a slow-moving mobile platform is another channel for medical companies to increase interaction and feedback. At the same time, the patient's behavioral preference and medication habits of the mobile medical platform have greatly realized the value of human-computer interaction and big data analysis, and rapidly improved the service efficiency and quality of the terminal patients.

In fact, this is also related to the dilemma faced by mobile medical care. When mobile medical or Internet medical services face C-side customers, the most prominent problems are data and business scenarios. From the perspective of business scenarios, it is necessary to give advice, consultation, diagnosis and management to patients. It depends on the understanding of patients, and it is impossible to achieve face-to-face communication. After the traffic dividends gradually fade away, the cost of obtaining online platform-based enterprises is very high. High, it is difficult to accurately reach the target group.

The second is intelligent hardware. The innovation of devices and services brought about by digital medical care provides patients with the convenience of self-management and enhances patient compliance. For the major disease of diabetes, a milestone event is the birth of Novo Nordisk. When patients can treat themselves, the burden of basic medical care will be much reduced, opening up the era of patient self-management.

As the collection of physiological indicators data of chronically ill patients, intelligent hardware is widely used in the fields of chronic disease treatment, monitoring, data collection, management, feedback and reminding, especially in the fields of diabetes and cardiovascular diseases. In the process of seeking medical care for chronically ill patients, it is usually necessary to repeatedly run hospitals or medical institutions to ensure the stability of the disease. The intelligent hardware self-tests the key indicators to promote the patient's medication compliance to a certain extent. At the same time, the smart hardware supporting APP is often also for patients. The best choice for education and interaction with patients. In addition, the patient's big data is also a valuable asset for pharmaceutical companies.

It is difficult to collect data from patients at the out-of-hospital-re-diagnosis stage. CFDA-certified data can be directly applied to clinically diagnosed smart hardware scarcity. For pharmaceutical companies, invest in a class of certified smart hardware. It is also a good business.

The third is offline service. Offline services are the main business of drug delivery and O2O services. It is difficult to manage chronic disease on the Internet. Online problems such as user compliance, treatment and exercise combined with chronic disease management cannot be ignored.

Wen Xiaoling, general manager of Juzhishou Health Management Co., Ltd. (former general manager of Tianshili Group E-Commerce) once expressed this view in public: “The payer decides the trend of the future pharmaceutical industry.†And two of the current payers are important. The role of medical insurance and industry, Tasly in 2011 with the Tianjin Municipal Human Resources and Social Security Bureau cooperation drug delivery project, opened the chain of patients to order-delivery-medical insurance payment, the first to try the optimization of the entire process of online prescription drugs, And in the pharmacy to increase the health testing services to achieve accurate marketing of drugs.

In the era when the online bonus has gradually disappeared, O2O (Online to Offline) will evolve into OMO (Online Merge Offline), and the online and offline integration supply and services have undergone tremendous changes. The only constant is better. To meet the needs of patients more quickly, especially the need for convenience. The management of chronic diseases in the future is more likely to be a form of online and offline integration. Online as a tool for patient education, compliance supervision, communication between the server and the patient, and assistance to offline services.

What is the effectiveness of drug sales + chronic disease services?

According to iResearch, the complete closed-loop management system consists of five major roles: mobile medical care, doctors, medical and health institutions, pharmaceutical companies, insurance, and collaborative services for chronically ill patients. It is generally believed that Internet medical companies and medical information companies are the main drivers of medical transformation, but in fact, in the market divided by demand, pharmaceutical companies that mainly sell drugs are in contact with demand, which is the most extensive category of patients. enterprise.

Through the following two cases, let us observe how the pharmaceutical companies' layout in chronic diseases is effective:

Tasly: ​​Get through the patient-drug-medical payment link and harvest 100,000 diabetic members

In September 2013, Tianjin launched a drug service project for patients with special diseases in diabetes clinics. This program allows people over the age of 60 to enjoy the convenience of online medicine purchase and medicine, and enjoy the current medical insurance reimbursement policy. Tasly's role in this is the service provider of information network technology providers, drug reservations and distribution.

According to the data of Tasly's 2017 annual report, the Tasly Diabetes Chronic Disease Management Platform has collected nearly 100,000 patients. In 2017, it achieved sales of 345 million yuan, a year-on-year increase of 53%, and sales increased 10 times year-on-year. At the same time, it achieved a reduction in the proportion of hospital medicines, and also saved tens of millions of expenses for Tianjin medical insurance.

In 2017, in order to improve the operational efficiency and service quality of the platform, Tasly has iteratively upgraded from the perspectives of drug distribution, value-added services, and introduction of big data systems.

The pharmaceutical distribution terminal is directly connected with the hospital prescription, and the drug delivery is successfully realized from the distribution center to the patient; through the drug QR code traceability system, the problem of accurate drug use and drug supervision is successfully solved.

The value-added service terminal, the company around the Tasly Pharmacy store, opened a number of chronic disease health management centers, providing existing users with monitoring, screening, pharmacy and other offline services, reducing the daily inconvenience of the hospital for patients, but also Saved a large number of registration fees and medical treatment fees for Tianjin Medical Insurance, and improved the efficiency of the use of medical insurance funds. The big data server gradually builds the chronic disease PBM (pharmaceutical welfare management) model, and through the connection of the hospital HIS (hospital management information) system, it realizes the transfer of prescriptions with more than 10 mainstream diabetes hospitals in Tianjin, and reaches the outside of the prescription hospital. Through the docking with the medical insurance settlement department, the patient truly realized the online medical insurance card settlement.

Through the Internet + model, and through the online medical insurance payment, offline pharmaceutical distribution of Chinese pharmaceutical companies, patients, hospitals, medical insurance new service model makes the Tasly Diabetes Chronic Disease Management Platform the only designated pilot project in China by the Ministry of Human Resources and Social Security. Thanks to the success of the platform in the Tianjin area, Tasly is actively promoting the replication of this model in multiple provinces.

Tonghua Dongbao: acquisition and self-construction "two-pronged approach", effectively managing more than 200,000 patients

The main product of Tonghua Dongbao is recombinant human insulin injection (trade name: Gan Shulin). Before the market of its recombinant human insulin products, 99.9% of the market share was monopolized by foreign companies. After the products went on the market, Tonghua Dongbao reorganized human insulin sales. At present, it has occupied more than 20% of the market share, ranking second.

Based on its own business chain, Tonghua Dongbao's diabetes chronic disease management platform includes drug treatment (insulin, Ypsomed pen and needle; other oral treatments such as oral administration), blood glucose monitoring (Huaguang Biotech, Red Heart App), patient behavior Management (your doctor app) is a combination of doctors, patients, platforms, and monetization channels (drugs, devices, services, etc.).

Through the "Your Doctor" APP in cooperation with Shanghai Orange Medical Network Co., Ltd., the viscosity of doctors and patients is enhanced, and the strategic goal of "insulin + blood glucose monitoring equipment + Dongbao Diabetes Platform" is realized through the integration of medicines, devices and mobile Internet.

According to the 2017 annual report data, as of the end of 2017, more than 9,000 endocrinologists have used the platform to effectively manage more than 200,000 patients, and more than 750,000 patients benefited from the platform. On the other hand, Tonghua Dongbao uses a comprehensive marketing model based on chronic disease management to provide a comprehensive solution for diabetes insulin therapy, and stimulates human insulin products, ultra-thin insulin injection pen needles, blood glucose monitoring test papers, etc. Product sales grew.

Figure 6 2017 Tonghua Dongbao Diabetes Product Sales (Source: Tonghua Dongbao 2017 Annual Report)

Through a series of service layouts, Tonghua Dongbao has created a total diabetes solution provider. The diabetes chronic disease management platform around “diabetes treatment, blood glucose monitoring, and patient behavior management†has been established. Tonghua Dongbao has also gradually transformed from medicine to medicine. A total solution provider for insulin therapy in diabetic patients.

When diabetics learn to test their own blood sugar, take hypoglycemic agents, fight insulin, and what about hospital doctors? This is the core overview of the importance of medication compliance in patients with chronic diseases. In fact, not only patient education, but also doctor education is a big problem for pharmaceutical companies. Therefore, through a series of service layouts, pharmaceutical companies can The cooperation of mobile platforms, smart hardware and even medical institutions complement each other.

The advantages of its own business line will help pharmaceutical companies to play a core competitive advantage in the process of chronic disease and Internet medical transformation. The ultimate goal of major pharmaceutical companies is to better market and sell. Therefore, in the service layout, Internet companies, pharmaceutical companies, and medical and medical companies work together to explore more precise treatments and more effective management methods.

Challengers in one area may be replaced by innovative traditional companies. When mobile applications are preparing to subvert the self-management of chronic diseases, they are bound to bear the operating costs of the disappearance of the Internet dividend.

On the other hand, pharmaceutical companies are working hard on chronic disease services, and the innovative service model is equivalent to being both a "chicken with raw eggs" and a "cooking cook" to enhance the patient's experience. Why not?

Ventilation is one of the most important components in a successful greenhouse.

If there is no proper ventilation, greenhouses and their growing plants can become prone to problems. The main purposes of ventilation are to regulate the temperature and humidity to the optimal level, and to ensure movement of air and thus prevent build-up of plant pathogens (such as Botrytis cinerea) that prefer still air conditions. Ventilation also ensures a supply of fresh air for photosynthesis and plant respiration, and may enable important pollinators to access the greenhouse crop.

Greenhouse Circulation Fan,Greenhouse Ventilation Fan,Automated Greenhouse Ventilation Fan

JIANGSU SKYPLAN GREENHOUSE TECHNOLOGY CO.,LTD , https://www.greenhousehydroponic.com